10 Best Gold IRA Companies 2023

Which Gold IRA companies offer you the best value for your dollar in 2023.

If you are considering rolling over your 401K into a Gold IRA you should ensure your retirement saving are in the right hands.

Not all Gold IRA companies offer the same services for all levels of investments. Some Gold IRA companies have high minimum investment criteria.

Here are some things you should consider before you contact a company and trust your hard earned savings or diversify your investment portfolio.

- Which Gold Company can you trust?

- Which Precious Metals Company has the most experience with these types of accounts, and the best service to their clients?

- What are the minimum requirements for a Gold IRA at each company ?

That’s why we have thoroughly researched this industry and found the few companies meet our strict requirements for excellence

Gold IRA Review delivers the the best companies we have found through our research and feedback from our readers that have invested with these companies based on our recommendation. We will also point out the pitfalls and which Gold IRA companies your should avoid with your retirement saving

Augusta Precious Metals

August Precious Metals are an Award-winning “Best Gold IRA Company,” singled out by Money magazine and others notable industry Magazines

Exceptional level of customer service:

Exceptional level of customer service:

1000s of top ratings

1000s of top ratings

100s of customer reviews, and endorsements by conservative talk show hosts and hall of fame quarterback Joe Montana.

Known for one-on-one educational web conference designed by on-staff, Harvard-trained economic analyst.

Allegiance Gold is our Gold Winner for 2023

Company has been experiencing massive growth

Dedicated “Learning Center” available on company website

Over a decade of precious metals industry experience

Customer services is top in the industry

Partners with top-rated IRA service providers for retirement investors

Goldco

Goldco is our Silver Winner for 2023

Best Gold and Silver Deal Prices

100% FREE IRA Rollover

A+ Better Business Bureau, AAA rating from Business Consumer Alliance

No high pressure sales tactics

Extensive Educational Resources

American Hartford Gold

Lowest minimum Gold IRAs

Buyback Commitment

Customized Plans

Top customer review

Birch Gold Group

Best Gold and Silver Deal Prices

100% FREE IRA Rollover

A+ Better Business Bureau, AAA rating from Business Consumer Alliance

No high pressure sales tactics

Extensive Educational Resources

Oxford Gold Group

Best For beginners in Gold IRAs

Site has resource library for investors

Information geared towards educating novice investors

Customers can access their account online

Patriot Gold Group

Minimum Investment: $10,000

Most IRA’s Qualify for “No Fee For Life” IRA

Diamond Sponsored A+ BBB Rated

Low-Cost Bullion, IRA Eligible, and Numismatic Coins Available

Lear Capital

Free IRA set-up and storage + no fees on buy-backs.

Exclusive 24-hour no-risk purchase guarantee

Price Match Guarantee + no-fees on buy backs

$3 billion in transactions & over 90,000 satisfied customers

Best For beginners in Gold IRAs

Site has resource library for investors

Information geared towards educating novice investors

Customers can access their account online

How Does Gold IRA Work?

How Does a Gold IRA Work?

A Gold IRA works exactly like any retirement account with the added benefit that it provides you more control over your investment to include physical gold coins and bars and other IRS approved silver, platinum and palladium metals.

Similar to any retirement account, with your Gold IRA or Custom Precious Metals IRA, you will be investing your retirement funds based on specific tax treatment (pre-tax or after-tax) and then take distributions in future. With your Gold IRA or Custom Precious Metals IRA, you will continue to have beneficiary (ies), receive quarterly statements and be able to log in online to check your balances

How Does a Gold IRA Work?

A Gold IRA works exactly like any retirement account with the added benefit that it provides you more control over your investment to include physical gold coins and bars and other IRS approved silver, platinum and palladium metals.

Similar to any retirement account, with your Gold IRA or Custom Precious Metals IRA, you will be investing your retirement funds based on specific tax treatment (pre-tax or after-tax) and then take distributions in future. With your Gold IRA or Custom Precious Metals IRA, you will continue to have beneficiary (ies), receive quarterly statements and be able to log in online to check your balances.

Types of Gold IRA Accounts

As with conventional retirement accounts, there are few types of accounts that each provide distinct tax benefits. The following are the three types of Gold IRA Accounts:

Traditional Gold IRA:

A traditional gold IRA is a tax-deferred retirement savings account and works just like pre-tax traditional IRAs when it comes to taxes. Your contributions and any gains will not be taxed and, in most cases, contributions are tax deductible as well. The IRS sets annual contribution limits of $5,500 if you are under 50 and $6,500 if you are above 50. With a pre-tax IRA you will have to pay taxes on your distributions during retirement.

Roth Gold IRA:

A Roth Gold IRA is an after-tax retirement savings account and works just like any Roth IRA. While there is not any upfront tax deduction with Roth IRA contributions, the main advantage of a Roth IRA is that you won’t have to pay any taxes down the line when you start to take distribution during retirement.

SEP Gold IRA:

SEP gold IRAs are available to business owners and self-employed individuals. The SEP Gold IRA works similarly to a pre-tax traditional IRA, in that your contributions are not taxed, but it offers higher contribution limits. Instead of the $5,500 limit, you can contribute up to 25% of your income or $53,000, whichever is less.

Gold IRA Review can help you navigate regulatory requirements, avoid tax pitfalls and diversify with physical precious metals to stabilize your retirement portfolio.

Does My Account Qualify?

Majority types of retirement accounts are qualified to be transferred all or portion, on a tax-deferred, penalty-free basis, into a Gold IRA or a custom precious metals IRA.

While traditional IRA, Roth IRA, Simplified Employee Pension (SEP) IRA, and Savings Incentive Match Plan for Employees of Small Employers (SIMPLE) are free of any rollover restrictions, others such 401k, 403b, 457b and Thrift Savings Plan (TSP), are qualified to be transferred if the individual is over 59 ½ years old or no longer works with prior employer.

Most accounts can be transferred on a tax-deferred, penalty-free basis with the exception of annuities which could, depending on the contract, have a surrender charge. However, an experienced IRA specialist will help you uncover if there are any surrender charges.

A verified Gold IRA Company we make the process of protecting your investment with precious metals easy. A team of an IRA specialist and a Senior Portfolio Managers will help you throughout the process and handle all the paper works.

Setting Up a Gold IRA Account

Setting up a Gold IRA is very simple. Opening your account can be either completed online by clicking the following link or through a physical application.

Your Gold IRA representatives are there to assist you every step of the way.

Fund Your Gold IRA

With your application completed and your self-directed IRA open, funding your Gold IRA cannot get easier. Funding the account is simple and can be completed by one of the three methods:

IRA Transfer:

The new IRA can be funded through an IRA to IRA transfer by simply completing a Transfer Request Form. This will ensure that the transfer is completed on a tax-deferred and penalty-free basis.

IRA Rollover:

A direct rollover from a 401(k) or other qualified retirement plan is another way to fund your self-directed IRA on a tax-deferred basis.

Cash Contributions:

To fund the account with cash, the self-directed custodian will accept either a check or wire. The taxable treatment depends on the type of the IRA account either pre-tax (traditional) or after-tax (Roth) basis.

One of the few limitations on funding your account is that you can’t legally fund it with gold coin or bullion you already own, in part because the U.S. government only allows certain coins and bullion to be held in IRAs.

Once the funds are received by the new self-directed IRA custodian, your Gold IRA representative will help you select the IRS approved coins and the depository to store your precious metals. Most designated Gold IRA associates, both an IRA specialist and a Senior Portfolio Manager, will manage the entire process of setting up and funding your Gold IRA or custom precious metals IRA.

IRA Approved Coins

A gold IRA or a custom precious metals IRA cannot hold just any type of physical gold or precious metals. With the Taxpayer Relief Act of 1997, the IRS approved the following four main precious metals to be invested into an IRA: gold, silver, platinum and palladium. With each type of metal, the IRS only allowed a select few forms of bullion, coins, rounds and bars. In an effort to focus on investment grade liquid products and limit collectibles older types of coins, the IRS issued requirements of fineness for the precious metals products. One reason for being selective is to ensure that the gold and other precious metal products meet minimum requirements likely to ensure better long-term value.

The following coins and bars are among those that meet IRA investment requirements. Gold coins and bullion must be 99.5% finess or higher.

- American Eagle and

- American Eagle Proof coins

- American Buffalo coins

- Canadian Maple Leaf coins

- Canadian Polar Bear & Cub

- Canadian Polar Bear

- Canadian Arctic Fox

- Austrian Philharmonic coins

- Australian Kangaroo coins

- British Britannia (2013 and newer)

- Chinese Panda coins

- Credit Suisse bars and other bars and rounds produced by an NYMEX or COMEX-approved refinery

- Silver coins and bullion must be .999 fineness or higher.

This list is not all-inclusive, and we know determining whether precious metals are appropriate for IRA investments can be tough, which is why our Allegiance Gold account executives are always ready to provide assistance.

Depository Storage

If you are interested in rolling the funds in your traditional IRA into physical precious metals, you must decide how you wish to store them before funding a Self Directed IRA. Your Allegiance Gold account executive will answer any questions you may have and help you determine which type of storage will work best for your retirement savings needs.

Depository Storage Facility for IRA

A Depository Storage Facility is a third party storage facility where all precious metals in storage are insured. With depository storage, your precious metals are stored in a high-security facility that’s 100 percent insured against all loss, damage, theft or other liability These Depository Storage facilities have highly advanced security mechanisms and tools such as timed locks, 24 hours monitoring system, automatic relocking, and vibration, motion, and sound detectors. All depositories provide all risk insurance and maintain a $1 billion insurance coverage through Lloyd’s of London.

According to the IRS, gold and other precious metals in a retirement account are required to be stored in the custody of an IRS-approved custodian at a third party storage facility until the funds are withdrawn on reaching the predefined retirement age. Putting your precious metals in depository storage ensures that they are fully protected

There is an added layer of security with any depository. When a depository receives any products, it will first inspect, audit, confirm, key in the product annotating the type, quantity and weight and then securely store the precious metals products.

Top Three Depository Storage Facilities:

- Delaware Depository (Wilmington, Delaware)

- International Depository Services

- Brinks (Los Angeles, CA or Salt Lake City UT)

Commingled Vs. Segregated Storage

Precious metals stored in a commingled storage option are held in a communal area along with other people’s products. Precious metals kept in segregated storage will be separated from all other precious metals at the depository in a storage compartment reserved for private use. Both segregated and non-segregated storage provide an equally strong degree of protection.

There are two options of storage:

Commingled:

A commingled storage in a Gold IRA or a Custom Precious Metals IRA simply means that your precious metals will be held in a segregated storage area based on the custodian but will be commingled with other customers within the storage area. When you later decide to sell, exchange or take an in-kind distribution of your precious metals, you will receive “like” precious metals and not the exact metals that you initially purchased.

Segregated:

A segregated storage in a Gold IRA or a Custom Precious Metals IRA ensures that your precious metals will be held in a separate storage area and will be segregated, marked and stored with your name and IRA account number. When you later decide to sell, exchange or take an in-kind distribution of your precious metals, you will receive the exact metals that you initially purchased.

What Is a Gold IRA

What is a Gold IRA?

A Gold IRA is an IRS-approved retirement account that functions in the same way as any regular IRA.

Unlike conventional retirement accounts such as IRA and 401(k) accounts that limit your options in standard paper-based assets such stocks, mutual funds and bonds, a Gold IRA allows you the added benefit of investing in physical Gold coins and bars and other IRS approved silver, platinum and palladium metals.

Benefits of a Gold IRA

By investing in a Gold IRA, you will diversify your retirement portfolio on a tax-deferred basis and maintain the tax preferential treatment. This means that transferring or rolling over a portion of your existing IRA account into a Gold IRA will not trigger any tax implications. Also, by opening a Gold IRA you can take advantage of an annual contribution of $6,000 if you are below 50 years old and $7,000 if you are above 50 years old. A trusted Gold IRA Company can help you navigate regulatory requirements, avoid tax pitfalls, and diversify with physical precious metals to stabilize your retirement portfolio.

By investing in a Gold IRA, you will diversify your retirement portfolio on a tax-deferred basis and maintain the tax preferential treatment. This means that transferring or rolling over a portion of your existing IRA account into a Gold IRA will not trigger any tax implications. Also, by opening a Gold IRA you can take advantage of an annual contribution of $6,000 if you are below 50 years old and $7,000 if you are above 50 years old. A trusted Gold IRA Company can help you navigate regulatory requirements, avoid tax pitfalls, and diversify with physical precious metals to stabilize your retirement portfolio.

3 reasons to invest in a Gold IRA:

-

True Portfolio Diversification

Investing a portion of your retirement in physical gold and precious metals diversifies your portfolio in an alternative uncorrelated asset that has a proven record of protecting your funds especially when markets, governments, and currencies falter. Wall Street’s investment vehicles are all paper-based, from stocks to bonds. Physical gold and precious metals provide an added layer of diversification.

-

Hedge Against Inflation and Deflation

Over time, inflation erodes your investments. Gold provides a hedge against both inflation and deflation and immune your portfolio from the effects of inflation.

-

Profit Opportunity:

Historical performance of gold shows that over the long run, precious metals have great profit potential. Case in point, in 2000, Gold was approximately $200 an ounce. Gold finished 2022 above $1,800 an ounce – resulting in a 6X return on investment.

Gold is a store of wealth and has a long history of achieving that purpose. Historical data shows that gold climbs in value through the years, even when economic times are tough, making it a valued addition to any well-rounded retirement portfolio. Financial experts use gold and precious metals as a hedge against inflation and deflation, dollar devaluation, and evolving negative economic and political environment.

Diversify and Preserve Your Assets with a Precious Metals IRA

Taking back control of your retirement savings is made easy. By opening a self-directed IRA with a Gold IRA company, you will be empowered to make your own investment decisions and choose IRS approved coins, bullion, and bars to invest in and carries the weight and security of real tangible assets.

Whether you’re looking to move existing employer-sponsored 401(k) accounts to more secure options or rollover portion of your existing traditional, Roth, or other types of IRA accounts into a Gold IRA, a Gold IRA company can help you navigate regulatory requirements, avoid tax pitfalls and diversify with physical precious metals that can help stabilize your retirement portfolio.

El último baile: Detrás de la tragedia de Monterey Park

Los Ángeles (CA) – Con una decena de disparos, Huu Can Tran, de 72 años, convirtió la localidad californiana de Monterey Park en el escenario del tiroteo masivo de mayor alcance de la historia del condado de Los Ángeles. La fatídica fecha, el 21 de enero de este año, acababa con más de una decena de muertos y otra decena de heridos ––muchos de ellos, personas de la tercera edad––. Horas después de la matanza, el agresor apretó el gatillo una última vez ––en esta ocasión, para quitarse la vida––.

Lo que había comenzado como una noche de festividades para celebrar el Año Nuevo Lunar en el Star Ballroom Dance Studio, un popular salón de baile al que acudían con frecuencia miembros de la comunidad asiática de la zona, rápidamente se transformó en la escena de un crimen que ha dejado a los residentes locales conmocionados.

A media milla del salón de baile vive Peter Ng, consejero delegado del Chinatown Service Center, quien a diario pasa por delante de éste y cuya organización se ha volcado en ayudar a las víctimas y a los familiares de éstas. “Esta tragedia…ha destrozado los corazones de todo el mundo”, lamenta Ng durante una presentación encabezada por AAPI Equity Alliance, Asian Americans Advancing Justice SoCal y Ethnic Media Services (EMS) el 26 de enero.

“En los años 70, (Monterey) era un punto de encuentro para los inmigrantes de Taiwán y China que iban a comprar y a comer a sus restaurantes”, dice. Y debido a su elevada población asiática, a esta localidad californiana se la conoce, de forma cariñosa, como “la pequeña Taipei” o “el Beverly Hills chino”.

Cuenta Ng que el tiroteo le obligó a enviar un equipo de especialistas al Centro de Trauma para atender a las víctimas y que han recibido llamadas de unas siete familias afectadas. Pero aclara que “la gente que necesita ayuda no es la que llama, sino sus familiares”. “Por ejemplo, la familia de la hermana de una víctima nos llamó porque estaba destrozada, se había encerrado en sí misma y no hablaba con nadie porque estaba traumatizada”.

Anuncia, además, un plan de “Reanimación Mental” dirigido a educar a la comunidad sobre el vocabulario y los comportamientos a los que se deben prestar atención para identificar si una persona puede requerir la ayuda de un especialista.

Recursos para las víctimas

Otra organización que saltó a la acción de forma inmediata fue AAPI Equity Alliance, que se alió con varias instituciones para poner a disposición de los afectados un directorio con los nombres y datos de contacto de entidades que ofrecen servicios psicológicos, apoyo jurídico y ayudas económicas a las víctimas y familiares de éstas.

Asegura Manjusha Kulkarni, directora ejecutiva de AAPI Equity Alliance, que el directorio se actualiza con frecuencia y está disponible en distintos idiomas asiáticos para facilitar el acceso a los recursos a la diversa comunidad inmigrante que procede de distintos países de ese continente.

Entre los múltiples programas de ayudas se encuentra también CalVCB, un fondo que, a los individuos que cumplan una serie de requisitos y previa presentación de varios documentos, reembolsa los gastos fúnebres, el tratamiento médico y la asistencia psicológica a las víctimas.

El sistema de CalVCB, sin embargo, no es fácilmente navegable, como apuntan otros panelistas. “Es un proceso muy burocrático y tarda meses”, asevera Connie Chung Joe, abogada y consejera delegada de Asian Americans Advancing Justice SoCal. “Nosotros les podemos ayudar a rellenar los formularios”. Sin embargo, tampoco hay garantías de que a los afectados se les apruebe la participación en el programa.

Otra de las iniciativas que se han puesto en marcha es una campaña de recaudación de fondos (GoFundMe) que, a 26 de enero de 2022, había logrado casi duplicar el objetivo inicial, fijado en $500.000.

Esta respuesta “es lo que realmente me ha dado esperanza”, asegura Chun-Yen Chen, directora ejecutiva del Asian Pacific Community Fund, que agrega: “toda la recaudación va para las víctimas y los supervivientes”.

Chen, cuyos hijos asistían de pequeños a clases de baile al mismo salón donde ocurrió el tiroteo, explica que ha recibido numerosas llamadas de miembros de la comunidad que “temen que el estudio de baile cierre sus puertas de forma permanente”. Su mensaje, en cambio, es que “necesitamos seguir bailando”.

Falta de coordinación entre el Gobierno y las organizaciones comunitarias

El tiroteo ocurrido en Monterey Park ha puesto también de manifiesto las deficiencias existentes en los sistemas de respuesta ante tragedias de esta magnitud. Como apunta Chung Joe, ha habido una desconexión y una falta de “coordinación entre el gobierno y las organizaciones comunitarias”.

Si bien el Gobierno tiene acceso inmediato a los nombres de las víctimas, esta información se blinda de cara a las organizaciones que brindan apoyo sobre el terreno, lo que dificulta garantizar que los recursos y servicios disponibles llegan a quienes los necesitan.

Por su parte, Chung Joe insiste en que esta desconexión se ve agudizada cuando el Gobierno trata de dar asistencia a las víctimas sin conocer cuáles son sus necesidades, barreras culturales y dificultades lingüísticas, datos que sí conocen de primera mano los centros comunitarios. Lamenta, además, no haber recibido una llamada de un representante político hasta el cuarto día después de la tragedia.

“He hablado con unos 100 representantes políticos a nivel federal, estatal y local…hasta que por fin he dado con la persona con la que necesitaba hablar”, dice Chung Joe.

Para terminar, la directiva expresó su descontento con las especulaciones emitidas por algunos medios de comunicación sobre el perfil y los motivos que llevaron al agresor a perpetrar un ataque contra su propia comunidad.

“No sabemos cuál era su intención, y me preocupa cuando escucho a los medios tratando de especular sobre lo que ha podido pasar y retratando a nuestros ancianos asiático-americanos de manera peligrosa o volátil”, denuncia. “Éste es el perturbador retrato que se ha visto a la luz de esta tragedia y de la de Half Moon Bay”.

Featured image: by Zedembee is licensed under CC BY-SA 4.0.

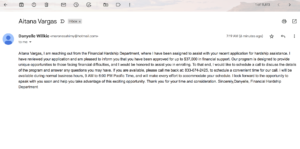

Beware of the Financial Hardship Scams

Los Angeles (CA) – As we come out of the pandemic, scams and identity theft continue to be rampant, and consumers need to be on their toes and know how to protect their personal information.

If you have received an email –like the one below– offering you $37,000 in financial hardship, unfortunately, it is a scam.

I, myself, just received one this morning. Not only does the Financial Hardship Department not exist, but the sender’s name (Danyelle Willkie) and email address do not match (maronesahimy@hotmail.com).

The recipients are asked to call the sender back on 833-674-2425. People being targeted are also reporting having received similar messages via SMS.

As appealing as the fake Financial Hardship Department’s offer may seem, it’s best to report the email as spam or phishing to your email provider or to your phone company.

For further information about scams, visit the FTC website: https://consumer.ftc.gov/features/pass-it-on

Featured image: by Got Credit is marked with CC BY 2.0.

V-Day lovers: Watch out for romance scams!

On a day like today, Investor News would like to raise awareness of romance fraudsters.

According to the FBI, romance scams occur when a criminal adopts a fake online identity to gain a victim’s affection and trust. The scammer then uses the illusion of a romantic or close relationship to manipulate and/or steal from the victim.

The criminals who carry out romance scams are experts at what they do and will seem genuine, caring, and believable. Con artists are present on most dating and social media sites.

The scammer’s intention is to establish a relationship as quickly as possible, endear himself to the victim, and gain trust. Scammers may propose marriage and make plans to meet in person, but that will never happen. Eventually, they will ask for money. Scam artists often say they are in the building and construction industry and are engaged in projects outside the US. That makes it easier to avoid meeting in person ––and more plausible when they as for money for a medical emergency or unexpected legal fee. If someone you meet online needs your bank account information to deposit money, they are most likely using your account to carry out other theft and fraud schemes.

Tips for Avoiding Romance Scams:

- Be careful what you post and make public online. Scammers can use details shared on social media and dating sites to better understand and target you.

- Research the person’s photo and profile using online searches to see if the image, name, or details have been used elsewhere.

- Go slowly and ask lots of questions.

- Beware if the individual seems too perfect or quickly asks you to leave a dating service or social media site to communicate directly.

- Beware if the individual attempts to isolate you from friends and family or requests inappropriate photos or financial information that could later be used to extort you.

- Beware if the individual promises to meet in person but then always comes up with an excuse why he or she can’t. If you haven’t met the person after a few months, for whatever reason, you have good reason to be suspicious.

- Never send money to anyone you have only communicated with online or by phone.

Listen to Special Agent Christine describe romance schemes.

Information by the FBI.

Simi Valley Man Sentenced to Over 4 Years in Prison for Fraudulently Obtaining More Than $1 Million in COVID Business Loans

LOS ANGELES – A Ventura County man who schemed with an Orange County man to illegally acquire disaster relief funds was sentenced today to 51 months in federal prison for fraudulently obtaining more than $1 million in loans intended to help businesses weather the COVID-19 pandemic’s economic fallout.

Manuel Asadurian, 66, of Simi Valley, was sentenced by United States District Judge Dale S. Fischer, who also ordered him to pay $1,071,222 in restitution.

Asadurian pleaded guilty in October 2022 to one count of wire fraud affecting a financial institution.

From April 2020 to January 2021, Asadurian and an accomplice, Jeffrey Scott Hedges, 51, of Irvine, schemed to fraudulently obtain federal disaster relief funds distributed through the Paycheck Protection Program (PPP) and Economic Injury Disaster Loan (EIDL) programs that Congress intended to help businesses during the pandemic.

Asadurian lied to the United States Small Business Administration and federally insured financial institutions on a total of 12 PPP and EIDL loan applications, which were submitted on behalf of Asadurian-controlled businesses, including LTL Enterprises LLC, Redline Performance LLC, and Diamond A Motorsports. Hedges submitted 18 fraudulent PPP and EIDL applications on behalf of companies he controlled, including West Coast Chassis, WCC Pro Touring, Von Schoff Apparel, and Hedges Corvette.

The false information submitted by Asadurian and Hedges included the number of employees to whom the companies had paid wages, the amount of payroll expenses for the companies, and false certifications that the loans would be used for permissible business purposes. In support of the bogus applications, Asadurian and Hedges submitted false tax documents, payroll records and bank records that fraudulently inflated the number of employees and amount of payroll expenses and gross receipts associated with the companies.

Once the PPP and EIDL loan applications were approved, they were deposited in bank accounts Asadurian and Hedges controlled. Asadurian and Hedges then used the fraudulently obtained loans for their personal benefit, including making mortgage payments on a personal residence, paying living expenses and medical expenses, and purchasing luxury vehicles.

In total, Asadurian sought approximately $1,620,122 in PPP and EIDL loans and fraudulently obtained approximately $1,071,222 related to those loans.

In a related case, Hedges pleaded guilty in August 2022 to one count of conspiracy to commit wire fraud affecting a financial institution and one count of aggravated identity theft for his submission of fraudulent PPP and EIDL applications that sought approximately $5,288,476. Hedges received approximately $2,087,701 of those loan funds. On January 30, Judge Fischer sentenced Hedges to a term of seven years in federal prison and ordered him to pay $2,087,701 in restitution.

The Federal Deposit Insurance Corporation Office of Inspector General; the Federal Reserve Board Office of Inspector General; the FBI; IRS Criminal Investigation; Treasury Inspector General for Tax Administration; and the Small Business Administration investigated these matters.

Assistant United States Attorney Scott Paetty of the Major Frauds Section prosecuted these cases.

Anyone with information about allegations of attempted fraud involving COVID-19 can report it by calling the Department of Justice’s National Center for Disaster Fraud Hotline at (866) 720-5721 or via the NCDF Web Complaint Form at: https://www.justice.gov/disaster-fraud/ncdf-disaster-complaint-form.

Press release by DOJ.

Featured image: by 401(K) 2013 is marked with CC BY-SA 2.0.

La economía, a examen. ¿A las puertas de una nueva recesión?

Los Ángeles (CA) – La pandemia más letal desde la mal llamada gripe española de 1918, no solo ha dejado una estela de muertes a lo largo y ancho del planeta. También ha puesto de manifiesto la vulnerabilidad de los sistemas sociales, ha desafiado la capacidad de respuesta del aparato sanitario ante una emergencia de gran magnitud y ha sembrado el temor a que una nueva crisis financiera sacuda los mercados y las bolsas de los principales motores económicos del mundo, incluyendo EEUU.

El ciclo de la pandemia se va cerrando y, con ello, están desapareciendo las medidas a nivel federal, estatal y local que protegían a los más vulnerables. Con la emergencia sanitaria contenida, se ha puesto fin a los programas de ayudas para los autónomos ––como PUA––, se están levantando las moratorias y los Gobiernos son menos propensos a tenderle una mano a quienes viven endeudados, carecen de un empleo estable o permanecen al borde del colapso financiero. Mientras la inflación sigue disparándose y el precio de la vida encareciéndose, los expertos valoran los retos económicos y los factores que podrían desatar una recesión este año.

“Todavía no estamos fuera de peligro”, aseguró Rakeen Mabud, economista jefe de Groundwork y directora gerente de Policy Research, durante un panel organizado por Ethnic Media Services (EMS) el 20 de enero.

La experta señaló que, sólo el año pasado, la Reserva Federal subió los tipos de interés siete veces y que, lo más probable, es que este escenario vuelva a repetirse. Se refirió, además, a las palabras de Jerome Powell –al frente de la institución–, quien ha admitido que todavía no se ha sentido el impacto completo de estas medidas.

Mabud recalcó que el “motivo real” que está alimentando la inflación en el periodo actual “no es porque la gente tenga más dinero en el bolsillo, o porque esté gastando demasiado”, sino porque vivimos en “un sistema construido por las grandes corporaciones que ha fracasado a la hora de satisfacer las necesidades de la gente en momentos de crisis”.

El bolsillo del consumidor, el mejor termómetro de la avaricia corporativa

La economista denunció, a la vez, la avaricia corporativa y las prácticas especulativas que se originaron en la pandemia, que continúan hasta la fecha, y que están asfixiando al consumidor. “Cualquiera que ha ido a comprar una docena de huevos al supermercado, ha visto la subida de precios”, aseveró.

Mabud descartó que estas subidas estuvieran causadas por gastos más elevados de producción, y lo achacó a las estrategias corporativas dirigidas a maximizar beneficios.

Entre las medidas para frenar y poner fin a este tipo de prácticas, Mabud sugirió que el Congreso introduzca regulación a nivel legislativo, y que el Departamento de Justicia (DOJ) y la Comisión Federal de Mercado (FTC) persigan a los especuladores.

Por último, advirtió que, fruto de las subidas de los tipos interés, la Reserva Federal puede ser la catalizadora de una recesión que deje a millones de personas sin trabajo. Pero también indicó que el paquete de medidas de austeridad promulgado por los republicanos, así como su política tributaria favorable a las grandes fortunas, suponen una segunda amenaza de cara una posible recesión.

¿Se sabe con certeza si habrá una recesión económica?

La sombra de una recesión es también una de las preocupaciones del economista George Fenton, analista sénior de políticas en el Centro para Presupuestos y Prioridades Políticas (CBPP). En su intervención, insistió en que no es posible predecir si habrá una recesión, y agregó que, de haberla, se desconoce su duración y su magnitud.

“El consenso es que, si tenemos una recesión, será corta y superficial. Pero podría ser corta y profunda, o larga y superficial. Realmente no sabemos con seguridad qué va a pasar”, aseveró.

Para evaluar el riesgo de recesión en EEUU, Fenton se apoyó en datos de Moody’s Analytics, que sitúan la probabilidad en un 50%. También citó una encuesta de Bloomberg a 40 economistas, la cual dibuja un escenario menos alentador, con una probabilidad del 70%.

El economista, además, señaló que en época de incertidumbre, medidas como los créditos tributarios por hijos son herramientas “muy importantes” para luchar contra la pobreza, y abogó por la continuación y creación de políticas similares que generen una mayor “seguridad económica”.

El crecimiento del mercado laboral “es insostenible”

Durante su turno de palabra, Wendy Edelberg, ex economista jefe de la Oficina Presupuestaria del Congreso y ahora directora del Proyecto Hamilton en la Institución Brookings, admitió estar “preocupada” por los “desafíos” que se avecinan este año.

Sugiere dar un paso atrás para evaluar con ojo crítico indicadores que, a priori, pueden parecer favorables. Entre ellos, la creación de 250.000 puestos de trabajo en diciembre de 2022. Asegura que este crecimiento laboral es tan potente que “es insostenible”, y recalca que, para evitar el descalabro económico, se tiene que producir una ralentización sistémica.

Para redondear su argumento, Edelberg sostiene que EEUU probablemente arrastraría al mundo a una recesión global si no logra sanear su deuda, y advierte de que los síntomas ya están ahí: Desde la caída de la bolsa en enero de este año, a la bajada de 275 puntos que experimentó el DOW.

Mientras tanto, hace una llamado a la reflexión para trabajadores y consumidores, ya que una de las tendencias que más preocupación le generan es que “estamos gastando (en la esfera del hogar y en la del trabajo) como si no hubiera una pandemia”.

Do you have any tips? Contact the reporter at aitana_investigations@protonmail.com.

Featured image: by David Paul Ohmer is marked with CC BY 2.0.