Amazon Says Independent Corporations on Its Platform Provided Over $4.8 Billion Worth of Objects Over Weekend

Amazon.com Inc stated on Tuesday Independent corporations selling on its platform crossed $4.8 billion in worldwide product sales from Black Friday by Cyber Monday, an increase of higher than 60% from a 12 months earlier.

In its first indication of effectivity for the 12 months’s peak on-line shopping for days, Amazon talked about higher than 71,000 small- and medium-sized corporations worldwide had surpassed $100,000 in product sales this trip season to this point.

The Seattle-based agency did not, however, give a breakdown of U.S. product sales or its private numbers for the weekend, nor for each of the two big shopping for days, saying solely that the holiday season whole had been its largest ever.

Latest enterprise estimates in a single day confirmed Cyber Monday on course to be crucial on-line shopping for day ever for america, garnering as a lot as $11.4 billion as a result of the COVID-19 pandemic prompted prospects to stay at residence and swap to the online for his or her trip shopping for needs.

The sturdy effectivity comes no matter virtually two months of gives since Amazon held its Prime Day product sales event in October, with retailers trying to find to recoup enterprise misplaced all through this 12 months’s coronavirus-driven closures of malls and outlets.

Within the meantime, Ottawa, Canada-based Shopify Inc talked about on Tuesday full Thanksgiving weekend product sales soared 76% to $5.1 billion, beating the sooner report of higher than $2.9 billion by Saturday evening.

“The report product sales … show the flexibility of the unbiased and direct-to-consumer corporations,” Shopify President Harley Finkelstein talked about.

Estimates from Adobe Analytics confirmed this 12 months’s conclusion to Thanksgiving weekend product sales would can be found in between $10.8 billion and $11.4 billion.

Whereas that was down from an earlier estimate of as quite a bit as $12.7 billion, it nonetheless merely surpasses this 12 months’s Black Friday decide of $9 billion, the strongest on-line product sales consequence for the day ever, along with remaining 12 months’s Cyber Monday full of $9.4 billion.

Purdue Pharma Pleads Responsible to Three Felonies Over OxyContin Misconduct

Purdue Pharma LP pleaded responsible to prison costs over the dealing with of its addictive prescription painkiller OxyContin, capping a take care of federal prosecutors to resolve an investigation into the drugmaker’s function within the U.S. opioid disaster.

Throughout a courtroom listening to carried out remotely on Tuesday earlier than U.S. District Decide Madeline Cox Arleo in New Jersey, Purdue pleaded responsible to a few felonies masking widespread misconduct.

The prison violations included conspiring to defraud U.S. officers and pay unlawful kickbacks to each docs and an digital healthcare information vendor known as Observe Fusion right here, all to assist preserve opioid prescriptions flowing.

Members of the billionaire Sackler household who personal Purdue and beforehand sat on the corporate’s board weren’t a part of Tuesday’s courtroom proceedings and haven’t been criminally charged. They agreed in October to pay a separate $225 million civil penalty for allegedly inflicting false claims for OxyContin to be made to authorities healthcare packages resembling Medicare. They’ve denied the allegations.

Assistant U.S. Legal professional J. Stephen Ferketic mentioned officers reserved the fitting to prosecute people related to Purdue, together with house owners, officers and administrators. Sackler relations have mentioned they acted ethically and responsibly whereas serving on Purdue’s board and have been assured the corporate’s gross sales and advertising and marketing practices complied with authorized and regulatory necessities.

Purdue Chairman Steve Miller entered the responsible plea on the corporate’s behalf and admitted to its prison conduct underneath questioning from Ferketic. Of the three prison counts in opposition to Purdue, two have been for violations of a federal anti-kickback legislation whereas one other charged the Stamford, Connecticut-based firm with defrauding america and violating the Meals, Drug and Beauty Act.

Purdue’s plea deal carries greater than $5.5 billion in penalties, most of which is able to go unpaid.

A $3.54 billion prison superb is ready to be thought-about alongside trillions of {dollars} in unsecured claims as a part of Purdue’s chapter proceedings.

Purdue agreed to pay $225 million towards a $2 billion prison forfeiture, with the Justice Division foregoing the remainder if the corporate completes a chapter reorganization dissolving itself and shifting belongings to a “public profit firm” or comparable entity that steers the $1.775 billion unpaid portion to 1000’s of U.S. communities suing it over the opioid disaster.

A sentencing imposing these penalties is ready to return across the time Purdue receives courtroom approval for a chapter reorganization.

Purdue earlier settled separate Justice Division civil claims, agreeing to a $2.8 billion penalty additionally anticipated to obtain little monetary restoration within the drugmaker’s chapter case.

Perdue Function in Opioid Disaster

The plea deal and different associated settlements have come underneath fireplace from Democrats on Capitol Hill calling for Purdue and its house owners to face extra extreme penalties for his or her alleged roles within the opioid disaster.

The corporate reaped greater than $30 billion from gross sales of OxyContin over time, enriching Sackler relations, based on U.S. and state officers. Since 1999, roughly 450,000 folks have died in america from opioid-related overdoses, based on U.S. knowledge.

Some two dozen state attorneys common have oppose right here the plea deal on the grounds that it successfully endorses a chapter plan they contend would entangle native governments with a public profit firm that continues to promote OxyContin.

Purdue, which filed for chapter safety final yr right here underneath an onslaught of litigation, has proposed settling 1000’s of lawsuits in a deal it values at greater than $10 billion. That’s contingent on donations of opioid reversal and dependancy therapy drugs it has underneath improvement and a $3 billion money contribution from the Sacklers, who would cede management of Purdue.

Along with the kickbacks and vendor scheme, between 2007 and 2017, Purdue ignored docs suspected of improperly prescribing opioids that have been flagged by its inner controls, and did not report OxyContin prescriptions from these physicians to the Drug Enforcement Administration as legally required, based on prosecutors.

A Purdue affiliate in 2007 agreed to plead responsible to misbranding OxyContin in a take care of prosecutors that resulted in about $600 million of penalties.

Shares Greater Thursday; Late Selloff Leaves S&P 500 Simply Shy of One other Report

U.S. inventory indexes closed principally increased Thursday after a late stumble pulled the S&P 500 simply in need of its third straight all-time excessive.

The benchmark index slipped 0.1% after spending a lot of the day increased. It’s on monitor for its second weekly achieve as Wall Avenue continues to coast following its rocket experience final month powered by hopes for coming COVID-19 vaccines. The Nasdaq composite set a file excessive for the second straight day. Treasury yields principally declined, a reversal from earlier within the week.

A few experiences on the economic system that have been higher than anticipated helped help shares. One confirmed that progress within the U.S. providers sector, together with well being care and retail, was barely stronger final month than economists anticipated. A separate report stated fewer U.S. staff filed for unemployment advantages final week than forecast, although economists cautioned the quantity could have been distorted by the Thanksgiving vacation.

Traders have additionally been inspired this week by indicators that Democrats and Republicans in Washington could get previous their bitter partisanship to achieve a deal to offer extra monetary help for the economic system. Home Speaker Nancy Pelosi and Senate Majority Chief Mitch McConnell spoke Thursday, a day after Pelosi signaled a willingness to make main concessions seeking a coronavirus rescue bundle. President-elect Joe Biden urged Congress on Wednesday to move a aid invoice now, with extra assist to return subsequent yr.

“There’s lots of optimism being constructed into the market proper now,” stated Sam Stovall, chief funding strategist at CFRA. “Traders are type of retaining their fingers crossed that we provide you with a stimulus bundle, irrespective of the dimensions.”

The S&P 500 slipped 2.29 factors to three,666.72. The Dow Jones Industrial Common gained 85.73 factors, or 0.3%, to 29,969.52. The Nasdaq composite added 27.82 factors, or 0.2%, to 12,377.18. Small firm shares made out higher than the broader market. The Russell 2000 index picked up 10.67 factors, or 0.6%, to 1,848.70.

Momentum throughout markets has slowed after the S&P 500 surged 10.8% final month on hopes that a number of coronavirus vaccines will get the worldwide economic system nearer to regular subsequent yr. The burst of optimism boosted shares of journey firms, banks and smaller companies specifically, after they have been among the many most harshly punished in the course of the pandemic.

“It’s fairly clear that buyers are taking a look at a few of these areas that may profit from a extra full reopening,” stated David Lefkowitz, head of Americas equities at UBS World Wealth Administration.

Now that inventory indexes are again at all-time highs, worries concerning the still-raging pandemic are making additional massive good points tougher. Governments all over the world are contemplating the approval of a number of coronavirus vaccines, and a U.S. rollout might start this month if regulators give their approval. Britain has already permitted emergency use of a COVID-19 vaccine developed by Pfizer and BioNTech.

However vaccines would initially exit solely to guard well being care staff and others at excessive threat. Within the meantime, coronavirus counts and hospitalizations proceed to surge. That has governments all over the world bringing again various levels of restrictions on companies and customers fearful about their very own well being. That, in turns, is threatening the financial restoration that obtained underway within the spring.

Throughout the nation, the Labor Division stated 712,000 staff utilized for jobless advantages final week. That’s an enchancment from the 787,000 of the prior week, but it surely nonetheless towers over the roughly 225,000 staff that have been making use of weekly earlier than the pandemic struck.

Considerations concerning the potential financial fallout from extra restrictions on companies has intensified the stress on Washington to ship extra assist. Nonetheless, Democrats and Republicans have been arguing for months with out a lot progress.

“Ideally we’d get some sort of fiscal help sooner fairly than later,” Lefkowitz stated. “The large information is there’s extra of a line of sight on the truth that the economic system will doubtless get again to full energy.”

On Wednesday, Federal Reserve Chairman Jerome Powell and Treasury Secretary Steven Mnuchin underscored the significance of such aid throughout a Home Monetary Providers Committee listening to. The economic system has been struggling extra since further unemployment advantages and different stimulus permitted earlier this yr by Congress expired.

Ralph Lauren led the gainers within the S&P 500 Thursday, vaulting 8.7%. A number of travel-related firms additionally completed close to the highest of the leaderboard, clawing again extra of their precipitous losses from earlier within the pandemic. American Airways Group rose 8.3%, Norwegian Cruise line gained 8.6, and United Airways climbed 6.8%. All three, although, stay greater than 40% decrease for 2020.

Boeing surged 6% after Eire’s Ryanair introduced that it’ll order 75 extra of the plane producer’s 737 Max jets, a vote of confidence for the troubled Max from one in every of Europe’s greatest finances airways. The airplane was grounded in March 2019 after two crashes killed 346 individuals.

The yield on the 10-year Treasury dipped to 0.91% from 0.94% late Wednesday.

European inventory markets closed principally decrease. Markets in Asia have been blended.

SEC Fines The Cheesecake Manufacturing unit for Deceptive Buyers on COVID-19 Enterprise Influence

The U.S. Securities and Exchange Commission stated on Friday it had fined restaurant chain The Cheesecake Manufacturing unit $125,000 to settle costs that it misled buyers in regards to the impression of the pandemic on its enterprise, the primary such case introduced by the regulator.

In March 23 and April 3 regulatory filings, the corporate stated its eating places have been “working sustainably” when in reality inner paperwork confirmed it was dropping roughly $6 million per week as a consequence of pandemic lockdowns and had solely about 16 weeks’ of money remaining, the SEC stated.

Though the corporate didn’t disclose this info with public buyers, it did share it with potential personal fairness buyers and lenders because it sought further liquidity, the SEC stated. The regulator’s probe additionally discovered that The Cheesecake Manufacturing unit didn’t disclose in its March submitting that it had already knowledgeable its landlords that it could not pay lease in April because of the hurt COVID-19 had inflicted on its enterprise.

The corporate stated in an announcement that it had “absolutely cooperated with the SEC,” and neither admitted nor denied its allegations.

Whereas Friday’s penalty is small, it underscores the regulatory dangers COVID-19 has created for public corporations wrestling with how finest to speak the pandemic’s impression, with white collar crime legal professionals predicting comparable SEC actions.

Final Could the SEC had requested public corporations that took emergency pandemic support to show they certified for the funds and had made constant representations to buyers about their want for the help.

“When public corporations describe for buyers the impression of COVID-19 on their enterprise, they need to converse precisely,” stated SEC Director of Enforcement Stephanie Avakian.

“The Enforcement Division… will proceed to scrutinize COVID-related disclosures to make sure that buyers obtain correct, well timed info, whereas additionally giving applicable credit score for immediate and substantial cooperation in investigations.”

Moderna Inc will have the ability to produce 500 million doses of its COVID-19 vaccine in 2021, Chief Government Officer Stéphane Bancel mentioned on Friday.

The corporate has submitted purposes in search of emergency use authorization in the US and the European Union after full outcomes from a late-stage examine confirmed the vaccine was 94.1% efficient with no severe security issues.

“For 500 million, I’m very comfy we’re gonna get there (2021),” Bancel mentioned on the Nasdaq Investor Convention.

He additionally mentioned the corporate would have the ability to preserve a premium value of $37 for its vaccine doses, though the premium is anticipated to fall to $25 for big-volume provides, such because the one to the U.S. authorities.

The Meals and Drug Administration is about to carry an advisory committee assembly on Dec. 17 to debate the corporate’s request for emergency authorization for its COVID-19 vaccine.

Bancel mentioned the corporate has seen renewed demand from many nations in search of further doses after it reported scientific knowledge.

Moderna coronavirus-19 vaccine

Earlier on Friday, Moderna prolonged its contract with the Israeli well being ministry to produce a further 4 million doses of its COVID-19 vaccine candidate.

The corporate mentioned on Thursday it will provide as much as 125 million doses of the vaccine by the primary quarter of 2021.

Reporting by Mrinalika Roy and Trisha Roy in Bengaluru; Modifying by Anil D’Silva, Aditya Soni.

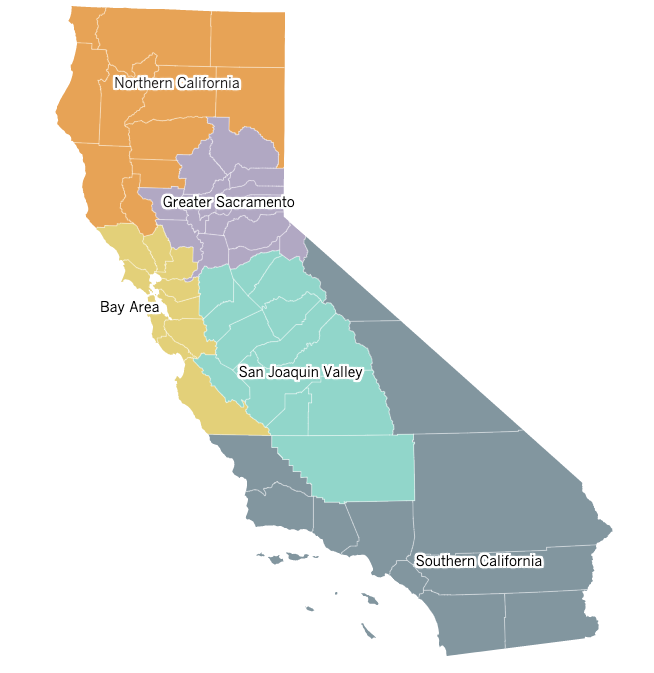

California heads into new stay-at-home order as COVID-19 cases overwhelm hospitals

A stay-at-home order will go into effect in Southern California and the San Joaquin Valley late Sunday, as COVID-19 cases soar and capacity at hospital intensive care units continues to drop.

The regions will implement the order Sunday at 11:59 p.m. Bars, wineries and personal-care services must close; restaurants must halt all dining; and gatherings of people from different households will be prohibited, the state confirmed. The rules will remain in place for at least three weeks.

The order — the latest in a series of attempts to slow the spread of the coronavirus and prevent local healthcare systems from becoming overwhelmed — is triggered when a region’s ICU capacity drops below 15%. Southern California’s ICU capacity Saturday was 12.5%, and the San Joaquin Valley’s was 8.6%, according to data released by the state.

Some 33 million Californians will be subject to the new order, representing 84% of the state’s population. They include residents of five Bay Area counties, which have decided to implement the stay-at-home order despite not yet reaching the threshold mandated by the state.

The order will be felt across Southern California but most dramatically in suburban counties like Orange, Ventura and Riverside, which have far less stringent restrictions than Los Angeles County, which imposed a modified stay-at-home order a week ago.

In addition to Los Angeles, Orange, Ventura and Riverside, the Southern California counties affected by the order are Imperial, Inyo, Mono, San Bernardino, San Diego, San Luis Obispo, Santa Barbara and Ventura. The San Joaquin Valley region covers Calaveras, Fresno, Kern, Kings, Madera, Mariposa, Merced, San Benito, San Joaquin, Stanislaus, Tulare and Tuolumne counties.

Hair and Nail Salons and Playgrounds close in LA

Affected communities will be required to close hair and nail salons, playgrounds, zoos, museums, aquariums and wineries. Overnight, short-term stays at campgrounds will be prohibited. Restaurants will be allowed to offer takeout service only.

Retail businesses will be limited to 20% customer capacity indoors, and stores will be required to ensure that there is no indoor eating or drinking.

Card rooms will be required to shut down, and hotels won’t be allowed to accept tourists.

Officials have said the measures are needed to avoid a crush of COVID-19 patients that could overwhelm the healthcare system, jeopardizing the ability to care for non-COVID patients as well. Mortality rates can dramatically increase when ICUs are stretched beyond capacity, and officials have warned that there are limits on the number of doctors, nurses and other healthcare providers who are well-trained in providing intensive care. Quality of care can fall substantially if hospitals are forced to transfer critically ill patients to parts of the hospital that are not designed for such use.

California has broken the record for COVID-19 hospitalizations for seven consecutive days, with 9,430 on Friday — more than quadruple the number from Oct. 24, when there were 2,254.

The state’s hospitals have never had so many severely ill COVID-19 patients; there are currently 2,182 in the ICU, the third consecutive day the record has been broken. During the COVID-19 surge in the summer, there were never more than 2,058 patients in the ICU.

In L.A. County, hospitalizations increased to 2,855 on Friday from 2,769 on Thursday. That number will likely continue to rise, as 49,000 people tested positive over the past week, and about 10% of them are expected to require hospital care, Barbara Ferrer, the county health director, said Saturday.

“That translates to close to 5,000 patients, and if even 20% of these patients need care in the ICU, they will require 1,000 staffed ICU beds,” Ferrer said in a statement. “This is our likely reality in two weeks.

“And if we all can’t get behind the existing directives to stay home as much as possible and avoid all nonessential activities and places where you are likely to be in contact with non-household members, we are likely to bear witness to one of the worst healthcare crises our county has seen in our lifetime,” she said.

In the San Joaquin Valley region, some hospitals are already strained.

Gov. Newsom New Stay At Home orders California

“We are at a point where surging cases and hospitalizations are not letting up,” Dr. Salvador Sandoval, Merced County’s public health officer, said in a statement.

The only hospital in San Benito County is “completely full,” Dr. David Ghilarducci, the county’s public health officer, said in a statement. “This is an alarming situation that could get much worse.”

Remote counties are dependent on neighboring areas for care, officials said, meaning that if one or two hospitals become overwhelmed, a domino effect could occur.

“Our mountain communities rely on the region for ICU-level care for COVID and other serious medical conditions, transferring our sickest to hospitals in the San Joaquin Valley,” said Dr. Eric Sergienko, health officer for Mariposa County and acting health officer for Tuolumne County. “These hospitals are stretched to capacity.”

Word of the new stay-at-home order came as California and Los Angeles County continued to set records for coronavirus cases reported in a single day.

With at least 43 deaths recorded Saturday, L.A. County is averaging 38 deaths a day, a pace not seen since late July.

The new stay-at-home order has faced criticism from all sides. Some say it’s too restrictive and will destroy small businesses; others question whether the rules are tough enough, wondering why malls are allowed to stay open.

Some local officials have also criticized the way the state has designated regions for the purpose of measuring ICU capacity. Officials of Ventura County noted that the Southern California region into which it falls is home to more than half the state’s population and are urging Gov. Gavin Newsom “to consider smaller, more targeted regions.”

San Luis Obispo County issued a similar statement, saying its ICU capacity is higher than that of most other counties in the Southern California region.

“We are disappointed to be categorized in the Southern California region and continue to ask state officials to reconsider our regional assignment to better represent the local ICU capacity,” said Dr. Penny Borenstein, San Luis Obispo County’s health officer.

Orange County Supervisor Lisa Bartlett said she supports a regionalized approach so that counties can assist each other if their hospitals fill up, but the state’s categories are simply too broad.

“Grouping 11 counties in Southern California into one region, particularly with one county that represents over 25% of the state’s population, is problematic,” she said, referring to L.A. County, the state’s most populous.

Bartlett noted that Orange County’s ICU capacity is more than 20%, compared with the regional availability of 12.5%. By being forced to shut down or reduce operations, she said, some business sectors, like restaurants and theme parks, are being “unfairly punished” by the new rules.

Keegan Hicks, owner of the Harbor Grill in Dana Point, said the popular restaurant was completely booked Saturday night. He said the restaurant will comply with the new order but believes there should be an exception for outdoor dining.

“We understand why these measures are being taken. We have nothing but concern and solidarity for frontline hospital workers,” said Hicks, whose family has owned the restaurant for 36 years. “But we believe that outdoor dining — as long as the restaurant is taking the proper protocols — is not responsible for the spread of the coronavirus.

“We’ve been open since May,” he added. “We have 60 employees and have had zero transmission among employees and zero customer complaints.”

Hilary Goldner, co-owner of Sweet 1017 Hairdressing in Seal Beach, heard the news about the order through text messages from her staff. After a busy Saturday, she is getting ready to close her salon for three weeks.

“It’s devastating,” she said. “We had had the two closures already, and this one comes at the busiest time of the year. Everyone is trying to move forward with their lives, and we play a role in that. It’s unfortunate and disappointing.”

Goldner said she understands that hospitals are getting slammed, but she doesn’t believe hair salons are contributing to the spread of COVID-19.

“We feel that we are already in compliance,” she said. “We’re in masks; our clients are in masks. We’re sanitizing. We’re going above and beyond for the safety of our clients.”

Orange County Sheriff Don Barnes said Saturday that deputies will not be dispatched to enforce compliance with stay-at-home rules or those governing face coverings and social distancing — as has been the department’s policy throughout the pandemic.

“Compliance with health orders is a matter of personal responsibility and not a matter of law enforcement,” he said in a statement.

Bartlett said she and Orange County Supervisor Don Wagner plan to introduce a resolution on Tuesday affirming the county’s commitment to advocating for local control to the greatest extent possible. She said county officials have been working with public health officers and hospitals to increase ICU capacity by such measures as reopening the Fairview Developmental Center as a field hospital to treat COVID-19 patients, which could potentially add 180 beds.

Still, she said, there’s “great concern” about what will happen in a few weeks, when cases may spike further due to the possibility of increased transmission from Thanksgiving gatherings.

“Based on our current ICU bed capacity, I think Orange County is in fairly good shape, but that could also change very quickly,” Bartlett said. “Our ICU bed capacity literally dropped 15% in one week. So we have to watch things very carefully.”

How to market an IPO Successfully with a Digital Marketing Campaign.

Companies need to let retail investors know that they are going public. Many companies hire Investor Relations companies that fail to reach the mark.

Building a company from the ground up, legal fees, and waiting to get approval for your Initial Public Offering means that the marketing company you hire to market should consider marketing your IPO just as seriously.

The Investor Marketing landscape is always changing as retail investors migrate gain more exposure. New niched investing websites are launched daily. These sites are built to gain subscribers not to promote a company.

The larger online financial websites Marketwatch, Bloomberg make it more difficult to get articles published, ads on the website, and content is now relying on sponsored content that is not written by their own staff.

Monthly packages for companies to engage these bigger sites start at $150,000 per month. That is a lot of money if the content will not be read by the right audience. Investor Leads has built a reputation with many online publications due to our extensive network that can help IPOs promote on more websites with greater stickiness.

How to Market an IPO Successfully?

Companies looking to market a successful IPO need a robust digital marketing strategy that builds on itself and is not a one-off email blast.

Here are some essentials for your successful IPO investor relations campaign:

A website that is up-to-date and professionally designed and created.

PDF and Powerpoints that are available on the site for download.

Press Releases that are well written and are distributed through a reputable company.

Email Content that is written by a highly-rated content marketer and legally checked over for anything that may cause issues.

Website content and sponsored content that is professionally written and compelling. This content needs to be informative and engaging not over sensationalistic.

Social Content that is legal and compelling, released at the correct time.

Retail investors are doing their due diligence online prior to the IPO and this is a perfect time to have all the relevant information online for retail investors to read and research.

Each of these essential investor marketing parts becomes the sum of the whole.

Success full Website techniques for an IPO

The company website should be designed and created with investor relations in mind. The website should not only look professional it should be built with a robust SEO strategy.

SEO is essential for marketing and IPO

Content for your website should have a goal. To entice potential investors, but without a successful SEO strategy how can investors find your company’s website online. SEO is not web design. It is as different as writing and drawing and it is important to understand how search engine optimization is going to help your IPO succeed.

SEO adds credibility to the IPO. A retail investor looking for information on the company needs to see that they are ranking high in Google and other search engines. Ranking in Google can take time and effort, thus savvy retail investors know that there is a real company that has taken their online presence seriously.

Content for the website should be clear and yet needs to rank well, otherwise what is the point in building content. Investors will have more confidence in finding content that is not just on the website but also has sources in other trusted online investing websites.

SEO is a strategy that needs serious attention in order to build a successful IPO, it cannot be stressed enough. Investor Leads delivers full SEO services to help build a company’s online visual presence.

Investor Relations Press Releases need an audience.

This should go without saying. Press Releases as it pertains to SEO is debatable, but Press Releases need and audience regardless. Using a poor quality Press release distribution channel is quite frankly a waste of time and money.

A Press Release schedule with updates that will reach a real retail investor audience will help build the visibility and branding for the IPO. A one-off Press release will not move your IPO needle. Investors who see multiple Press Releases are more likely to invest in a company after they see 2 – 5 Press Releases. This means that you may not see results immediately, but you will see results when you follow a long term strategy.

Online Advertising for your IPO

Banner ads on reputable online financial sites will help build a company’s IPO. To reach a new retail investor audience, it is important to build trust and familiarity with the IPO. Banner ads should be considered as an important part of the IPO strategy that drives potential investors to the website. Banner ads on reputable investing sites are still a valuable marketing technique for an IPO.

Native Advertising and Content Marketing for Investors

Building a full content marketing campaign will help an IPO build momentum fast. Retail investors read more content marketing articles and are 5 times more likely to invest than with traditional online marketing techniques. Creating content and native ad investor marketing campaign helps elevate the IPO and beat competition. Content marketing and Native ads are one of the best ways to market and IPO successfully.

Email Marketing

Email marketing to retail investors is still an essential process. With new laws in effect how email marketing to investors is conducted is important. Investor Leads delivers email marketing to opt-in can-spam compliant retail investors.

The SEC just changed Accredited Investor Definition. The biggest news in investing for years.

On August 28th, the SEC made a huge announcement that could change the way we invest forever.

Since the Securities Act of 1933 was passed, regular investors has been locked out of the private markets. This means only the super wealthy could invest early in companies like Facebook, Apple and Amazon.

WHY WERE REGULAR INVESTORS EXCLUDED FROM INVESTING AND GENERATING HUGE RETURNS LIKE THE HIGH-NET WORTH INDIVIDUALS?

According to the SEC guidelines, they didn’t have enough money to be recognized as an “accredited investor”.

SEC chairman, Jay Claton has been working to get these archaic laws changed to allow investors of all incomes to invest early in pre-IPO companies regardless of income.

“Today’s amendments are the product of years of effort by the Commission and its staff to consider and analyze approaches to revising the accredited investor definition,” said Clayton.

“For the first time, individuals will be permitted to participate in our private capital markets not only based on their income or net worth, but also based on established, clear measures of financial sophistication.”

The accredited investor definition was originally put in place to protect investors from harm, determining “financial sophistication” solely based on income or net worth doesn’t make much sense.

Chairman Clayton agrees:

“[W]e do not believe wealth should be the sole means of establishing financial sophistication of an individual for purposes of the accredited investor definition. Rather, the characteristics of an investor contemplated by the definition can be demonstrated in a variety of ways.”

These include the ability to assess an investment opportunity — which includes the ability to analyze the risks and rewards, the capacity to allocate investments in such a way as to mitigate or avoid risks of unsustainable loss, or the ability to gain access to information about an issuer or about an investment opportunity — or the ability to bear the risk of a loss.”

THE NEW ACCREDITED INVESTOR DEFINITION OPENS UP A LARGER POOL OF FINANCIALLY SOPHISTICATED INVESTORS AND WILL OPEN FURTHER DEFINITION IN THE FUTURE.

The certification, designation, or credential arising out of an examination or series of examinations administered by a self-regulatory organization or other industry body, or is issued by an accredited educational institution;

The examination or series of examinations are designed to reliably and validly demonstrate an individual’s comprehension and sophistication in the areas of securities and investing;

Persons obtaining such certification, designation, or credential can reasonably be expected to have sufficient knowledge and experience in financial and business matters to evaluate the merits and risks of a prospective investment; and

An indication that an individual holds the certification or designation is made publicly available by the relevant self-regulatory organization or other industry body.

REG D INVESTING WILL BECOME A HUGE INVESTMENT VEHICLE IN THE FUTURE.

Reg D investing is the best way for accredited investors to build wealth, through mini-ipo.

Under Rule 506(c) of Regulation D, a company can broadly solicit and generally advertise the offering and still be deemed to be in compliance with the exemption’s requirements if:

The investors in the offering are all accredited investors; and

The company takes reasonable steps to verify that the investors are accredited investors, which could include reviewing documentation, such as W-2s, tax returns, bank and brokerage statements, credit reports and the like.

Purchasers of securities offered pursuant to Rule 506 receive “restricted” securities, meaning that the securities cannot be sold for at least six months or a year without registering them.

Real Estate Investors looking for Reg D investments

THE DIFFERENCE BETWEEN RULE 506 (B) AND 506 (C) FOR REG D REAL ESTATE INVESTORS

With the Jumpstart Our Business Startups (JOBS) Act passing back in 2012, it is easier for non-accredited investors to invest. Most importantly, it was important for private offerings – it lifted an 80-year ban on public solicitation of private investments. Companies using Regulation D (Reg D) to raise capital are able to raise funds from accredited and non-accredited investors. For those who are confused about what that is, read this article about the basics of Reg D, and specifically Rule 506 of Reg D.

Reg D is a regulation governed by the SEC, maintaining private placement exemptions. This is opportunistic for smaller companies, as they can raise capital both faster and cheaper than releasing their company to the public. It allows capital to be raised through equities and debt securities without needing to register them with the SEC. One must still follow the requirements required by the state and federal government.

Companies and Investors must still follow guidelines, fill proper paperwork, and disclose important information. Companies must fill out a “Form D” electronically with the SEC. Although one must fill out the Form D, it is far less tedious than preparing for a public offering.

The company offering the private security must also provide disclosures about any “bad actor” events within the timeframe of issuing the security.

Importantly, Rule 506 of Reg D gives two distinct exemptions for companies offering securities. Through these exemptions, companies can raise an unlimited amount of money.

Rule 506(b) Reg D Offering

Rule 506 (b) is for an unlimited number of accredited investors and up to 35 non-accredited investors, who are labeled as “sophisticated”. To be a sophisticated non-accredited investor, one must have sufficient knowledge and experience in business and financial situations. By having said knowledge, they can be trusted to evaluate the cost-benefit analysis of a potential investment.

Under Rule 506 (b), the company offering the securities is not able to use general solicitation to advertise. Also, companies decide on what information they choose to disclose, so long as it doesn’t go against anti fraud regulations, and doesn’t include any false and misleading information. The company must be available for questions from potential investors.

Rule 506 (c) Reg D Offering

Reg D 506(c) is for accredited investors. Rule 506(c) of Reg D investments states that companies can broadly solicit and generally advertise a private offering, and still be within compliance of the requirements. It does state some prerequisites, such as requiring all the investors in the offer to be accredited investors and requiring the company to take the necessary and reasonable steps to verify the accredited investors.

If someone purchases securities related to the Rule 506 are given “restricted” securities – meaning those securities cannot be sold for at least six months to a year.

Rule 506(c) of Reg D also means that investors may invest immediately into a project, instead of waiting the cool-off period. An unlimited amount of investors may invest, raising an unlimited amount of money.

Another important event is the signing of the $2 trillion Coronavirus Aid, Relief, and Economics Security (CARES) Act. It allows grants and loans equal to 10% of the country’s economy. It could lead to tax breaks for potential investors, as well as support for smaller businesses.

Opportunity Zones

To qualify for the benefits that Opportunity Zones reap, one must reinvest one or more capital gains in a Qualified Opportunity Fund. This is described as an investment vehicle organized as a corporation that holds 90% or more of its assets in a qualified opportunity zone property, rather than another qualified opportunity fund. There are three tax benefits to reinvesting capital gains in a Qualified Opportunity Fund: first, there is a temporary tax deferral on any gains in a qualified opportunity fund within 180 days of realization; second, there is a 10% step up in basis for gains reinvested in a qualified opportunity fund if the investment is held for five years; third and finally, investors who invest in a qualified opportunity fund can exclude permanently from taxation any capital gains that accrue after their investment in a qualified opportunity fund, if the investment is held for at least 10 years.

In short, Reg D is something that needs to be looked into. The opportunities of investing through Rule 506 means that companies can raise unlimited funds through accredited and non-accredited investors by offering private securities through equities and debts. Rule 506(b) allows for an unlimited number of accredited investors and a maximum of 35 investors; Rule 506(c) is only for accredited investors, but the company can generally advertise their offerings to said investors. Additionally, the CARES Act offers tax refunds for those investing in businesses, as well as mortgage forbearance and an increase in grant funds. It is a very viable form of investing, and it benefits smaller companies as it allows those companies to raise the maximum amount of funds needed for operation at a cheaper cost. Overall, it is important for investors to take advantage of this opportunity to maximize their returns.

Uber and Lyft will shut down their ridesharing services in California on August 20th.

Drivers of Uber and Lyft are used as pawns by ridesharing company in an attempt to operate in California. Uber and Lyft should have been more proactive all along.

Both Uber and Lyft have decided to make this a messy divorce and seem like parents who have are using their kids as pawns in the courts. The problem is that the kids have grown up and are fed up with the arguing.

The ridesharing platforms have for years not even acknowledged their riders and employees, and have been negligent in many circumstances in taking care of safe working conditions at all levels.

While riders were heading out to clubs, restaurants and over to their latest tinder date for a Netflix and chill, Uber and Lyft decided that they were too big to fail.

This is a brand new world, COVID and Shutdowns has hurt the rideshare company but, more than that it has hurt the drivers, who are facing extreme hardship as a result of the drop in riders and trips.

It seems now Uber and Lyft want to act like they are the victims, being bossed around, but none of this is new to the world of contract employees in California. Now they are at an impasse and will effectively shut down in California on August 20th.

As usual, it is the Uber and Lyft drivers who will suffer. With many drivers using the driver app as a means to help pay rent, food, and basics, the Uber shut down will affect drivers the worst.

The Uber world of arrogance

Uber, has in the past been arrogant, they have been shut down in several countries and cities, for illegally operating their services.

Uber, has implemented work practices that have been frowned on by lawmakers and congress, but, as their meteoric rise to $72 billion valuations happened in 2016, the higher levels felt that they were untouchable.

Several key members of Uber’s C-level exes left the company prior to their 2018 IPO after many allegations were made public.

Uber and Lyft too little too late

Even after a decade, neither company has managed to turn a profit. The startups sold themselves to cities as creators of good jobs and providers of new transportation options. But the cities were hoodwinked by the fantasy, too — those jobs are precarious and low-quality; many workers hover around or below minimum wage and must clock dangerously long hours to hit ride targets and surge rates. Taxi drivers, meanwhile, were pushed out of business by the venture capital-fueled companies and are despairing. And city streets are more gridlocked than ever

After the ruling, both Uber and Lyft threatened to exit the state entirely if their legal appeals were defeated. Amazingly, this was less than 48 hours after Uber’s CEO Dara Khosrowshahi proclaimed in a New York Times op-ed that “gig workers deserve better.” If that means allowing the drivers who make his service possible to have basic employee benefits, though, he’d apparently rather shut the whole thing down.

Lyft meanwhile, was more straightforward in its appeal — it said that if it had to classify its workers as employees, it simply couldn’t afford to operate.

Uber — Shares of Uber climbed 0.4% after the ride-hailing company said it does not plan to shut its California Uber Eats operations due to the court case that forced it to suspend service in the state to reshape its business model. A judge recently granted a preliminary injunction requiring the company to reclassify drivers as employees, instead of contractors.

Uber and Lyft drivers have long complained about poor pay, lack of protections, and an inability to unionize to collectively bargain with the companies. There have been stories about drivers sleeping in their cars because they can’t afford to live in the cities where they work, struggling to make ends meet, and feeling totally at the mercy of a faceless algorithm that dictates when and where they drive and for how long.

Prop 22 Uber and Lyft

California is an obvious place for the line to be drawn in the sand. It’s where Uber and Lyft were founded and where they raised billions of dollars from investors before eventually going public. But neither company has ever been profitable. They both have actually set records for the amount of money lost in the run-up to their respective IPOs. And since going public, they have continued to bleed cash.

“Prop 22 is not just securing an AB 5 carveout for gig companies,” said Carlos Ramos, a 39-year-old Lyft driver based in San Diego and member of the pro-AB5 group Gig Workers Rising. “It is also designed by gig companies to ensure that these corporations are exempted from having to observe basic labor protections for workers for generations to come.”

Uber and Lyft have money to burn on advertising, a direct line of communication to their customers, and a willingness to lose tens of millions of dollars more to make their point. Going dark in one of its biggest markets in the country to really drive the message home about what’s a stake could be a gamble worth taking. Uber lost over $16 billion in the three years running up to its IPO. Since going public, it lost another $13 billion. By comparison, Lyft lost a measly $2.6 billion in 2019, but its business is based entirely in North America, while Uber is global.

Whatever money both companies will lose closing up shop in California could be pocket change compared to getting to rewrite the laws governing work in the state

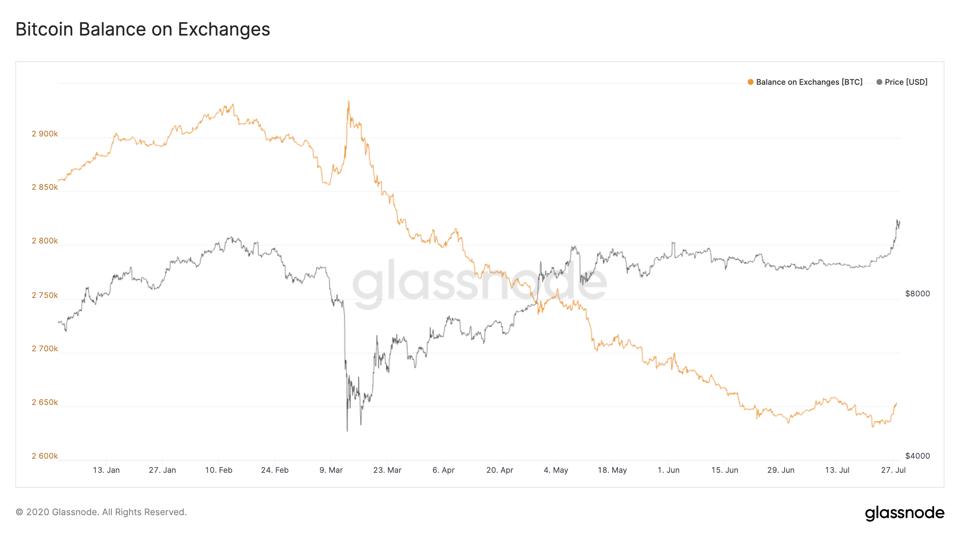

Bitcoin Briefly nears $12,000 But Crypto Investors Yawn

If a Bitcoin rally goes unnoticed, has the crypto investor markets been hyped to its limits?

Only the most rabid crypto investors seem to be following the mostly stagnant and deserted crypto markets.

Breaking through the $11,500-$11,800 range was the bulls most significant achievement of the last week and a number of analysts have noted that above the $12,000 level there is little overhead resistance.

Bitcoin hits highs breaking resistance level to a deserted landscape

This has led some traders to forecast a swift move to the $14,000-$15,000 level. This seems a little premature, less like a rise in Bitcoin and more a closed room of crypto investors talking.

This most recent move to $12,000 broke through this ‘ancient’ range and according to van de Poppe once “the price of Bitcoin breaks through this zone, then there is a lot of open range above and a new bull market will be upon us.”

If BTC surges past a level it failed to reclaim for years, it could indicate the formation of a potential bull run.

Traders also consider a critical resistance level as an area with large selling pressure. Once that level breaks, it could trigger an uptrend.

For sellers, there are three strong arguments to support a bearish scenario.

First, the Bitcoin market is currently heavily skewed to buyers. The overwhelming majority of the market are longing Bitcoin and other top cryptocurrencies.

Second, the funding rates of perpetual swaps are nearing levels that are not sustainable over a prolonged period.

Perpetual swaps are a type of futures contract that does not have an expiration date. It is also the most popular form of Bitcoin futures contract.

Funding rates of perpetual swaps across exchanges are surging because the number of long contracts is rising.

Third, the multi-year resistance at $11,500 could serve as an area for sellers to defend.

One Highly Optimistic Metric Suggests A Difficult Battle Between Bulls And Bears

While sellers have several viable reasons to be bearish, the exchange inflows of Bitcoin are not increasing.

The term exchange inflow refers to Bitcoin received by exchanges. Investors typically send BTC to trading platforms to sell and as such, exchange inflows often hint at heightened selling pressure.

Data from on-chain market analysis firm Glassnode spotted no large-scale deposits of BTC into exchanges. That could indicate that whales are not selling BTC yet.

A key resistance level at $11,500 and high funding rates could raise chances of a market cool-off. But investors are seemingly optimistic in the medium-term, and expect BTC to overcome it.